Tax Compliance (Submitting annual VAT returns)

In 1998, as part of the financial reform element of its Comprehensive Reform Program (CRP), Vanuatu introduced a Value Added Tax (VAT) that was imposed under the VAT Act No. 12 of 1998, at the rate of 12.5% on the supply of most goods and services. In 2018, this rate was increase by 2.5%. Vanuatu’s VAT was modelled based on the New Zealand’s GST regime operating with the current rates of 15% and 0% of tax and minimal exemptions. Value Added Tax is now administrated by the VAT ACT CAP [247].

Any business must register with the (VAT) office if it anticipates turnover of at least 4 million Vatu per year. Section 12 of the Act requires businesses to register with the VAT Office within 21 days of becoming liable to pay VAT.

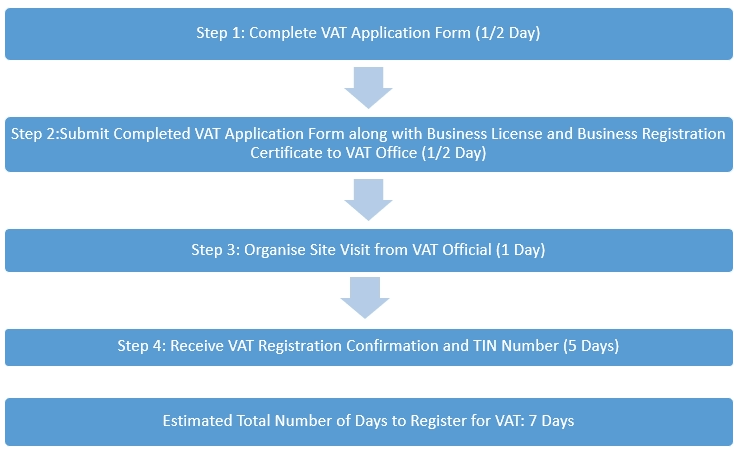

Steps for VAT registration

Step 1

Complete the application form available from the Department of Customs and Inland Revenue’s VAT office or from their website here:

https://customsinlandrevenue.gov.vu/images/Forms/VAT/VAT_Application_for_Registration_english.pdf

Step 2

Submit the completed application form along with a copy of a valid business license and business name registration certificate to the VAT Office. In the case of businesses not yet operational, a copy of the business plan must also be provided.

Step 3

If required, organise a visit from a VAT Office official to the physical site of the business.

Step 4

Receive a letter confirming VAT Registration and identifying the tax identification number (TIN Number), date of registration and when the first return is due, along with a VAT Guide and VAT book with 12 blank forms. A fee of 1,000 Vatu is charged for subsequent VAT books.

Forms required:

- VAT application form

- Copy of a valid business license (See Section 4)

- Business name registration certificate (See Section 3)

- Fees: No fee is charged for registering to pay VAT.

When and how should you submit your VAT returns

Registered persons are required to furnish VAT returns and pay the tax owing (if any) on the 27th day of the month following the end of their taxable period, except in the case of returns otherwise due on 27th December which are not required until 5th January of each year. For example: VAT for the month of June is due on the 27th of July.

You must submit and pay for VAT return in person at the Inland Revenue Taxpayer Services office, behind the Chinese Club. Payments can be made by cheque or cash.

Note: If a return due date falls on a weekend or public holiday, then the due date is shifted to the first working day after the weekend or public holiday. The normal taxable period is 1 month, however if a person’s taxable supplies are less than VT8 million a year they can apply to file 3 monthly (quarterly) returns.

What forms are required

Inland Revenue will refund VAT to you when the VAT you have paid is greater than the VAT you have collected.

Sometimes Inland Revenue is allowed to deny payment of a refund to you. Here are some situations where this may happen:

- A refund may be used to pay any other taxes you owe, for example, overdue business license fees.

- If you have not filed a return for any taxable period, Inland Revenue may hold your refund until you send the overdue return.

When submitting a VAT return, you simply need to provide your VAT book with the completed form inside. Your VAT return should contain your total sales and purchases for the period, the amount of VAT you owe and the amount you can reclaim, and what your VAT refund is.

You'll have to submit a VAT refund even if you don't have any VAT to pay or reclaim.

You can attach a cheque for the amount you owe with the booklet made out to the Vanuatu Government.

Penalty Fees

The new penalty regime was introduced in January 2020 for VAT returns, which are due for filing and payments on the 27th of each month.

If you fail to make payment of VAT on time, and/or you file your VAT return late, penalties and/or interest will be charged as follows:

If you file late:

- A late filing penalty of VT30,000 (for an individual) or VT50,000 (for an entity); and

- For each day that the return remains outstanding, a late filing penalty of VT3,000 (for an individual) or VT5,000 (for an entity)

If you pay late:

- A late payment penalty of 5% of the total that should have been paid; and

- For each day until payment is made, late payment interest at a daily rate of 20% per annum.